Discover Crypto Tax in Australia

GTP, CIBA

Updated:

Update Due:

Crypto Tax in Australia is a very hot topic as Australia is one of the countries in the world with a high crypto ownership rate. According to a survey released by Finder, the country ranks 3rd out of 27 countries, with 22,9% of Australians owning crypto.

As the number of crypto owners in Australia increased rapidly in recent years, the Australian Tax Office (ATO) has decided to watch those entering the crypto asset market. They are keeping track of all of their crypto-related activities in the country. Therefore, there is no escaping the tax obligation which rises from owning crypto assets.

The Australian Tax Office (ATO) and Crypto Assets

The Australian tax office does not define Bitcoin and other cryptocurrencies as money or foreign currency. Instead, they see them as intangible assets that can be acquired for long-term or short-term profits, giving rise to capital gains tax or income tax.

Bitcoin and altcoins attract both Capital Gains Tax and Income Tax in Australia. Australian Tax Office (ATO) has established that anyone who actively engages in the buying and selling of cryptocurrencies is obliged to declare any profits or losses made on such activities.

The Crypto Investor

The crypto investors’ goal is to build wealth over the long term. The goal is to buy and hold the asset for one or more years and then sell the asset after the increase in value. Profits will be subject to Capital Gains Tax. Losses can roll over and decrease your current year’s taxable liability.

The Crypto Trader

The crypto trader buys and sells cryptocurrencies frequently to produce income.

Even though both investors and traders are looking to make profits through market engagement, traders seek returns by buying and selling crypto assets over a shorter time frame.

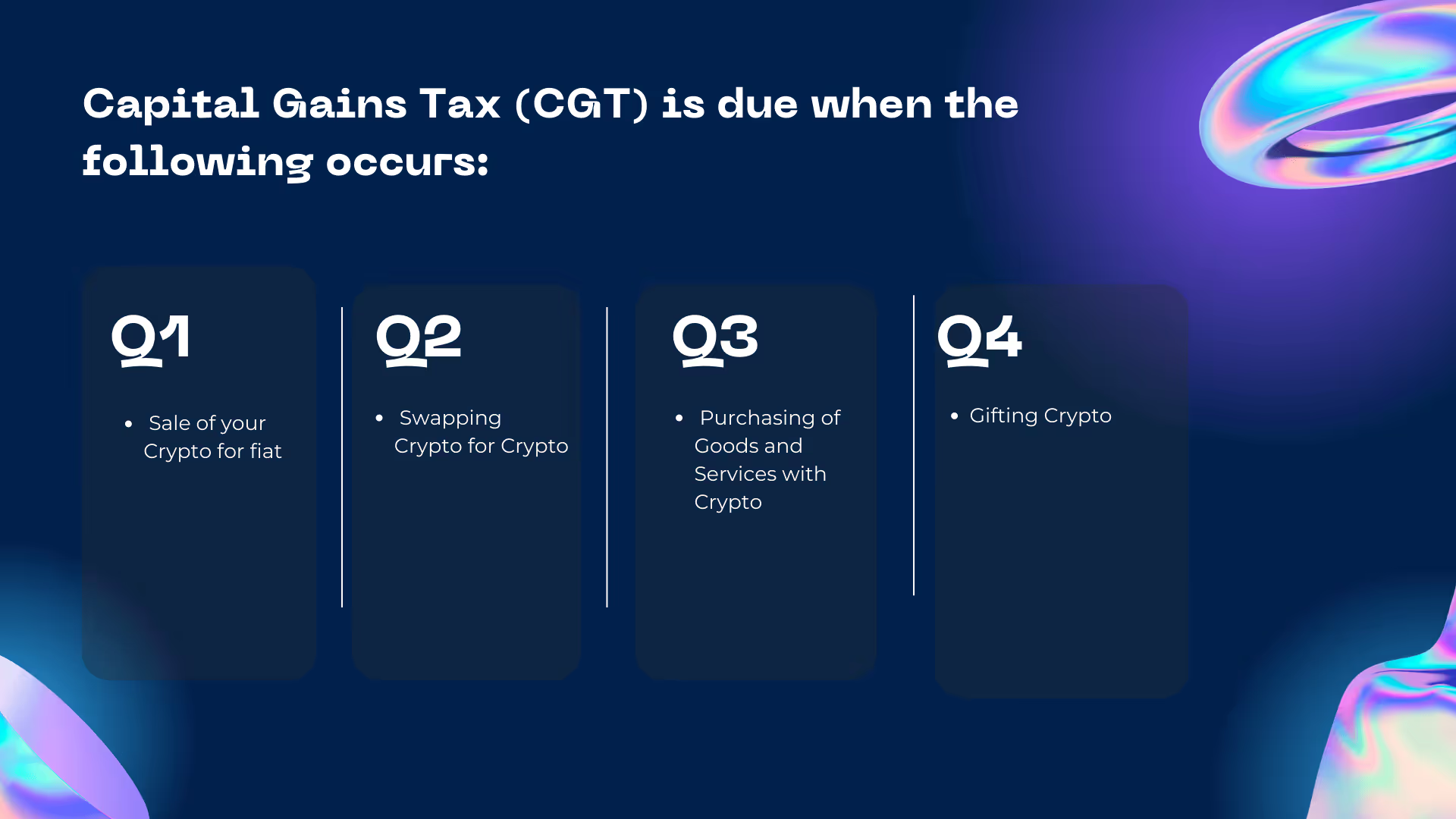

Capital Gains Tax Australia

When you dispose of any crypto asset, you must pay tax on the gains made from the disposal of such asset.

- As an Australian resident, you are entitled to a 50% capital gains tax discount if you held the asset for a 12 months period or longer.

- The percentage at which you will be taxed on regarding your capital gains tax will be the same as your income tax rate. Do remember your income tax rate will be dependent on your total income that you received during the tax year. Have a look at the ATO tax rate table here.

Use the following calculation to calculate Capital Gain:

Firstly you will need to know how to calculate the base cost. Use the following equation:

Base cost = Coin Cost + Fees (transaction fee/brokerage fees)

You can now calculate your Capital Gain amount:

Selling Price - Base Cost (Purchase Price) = Capital Gain

Example:

Chris bought 1 Bitcoin worth $11 000 in 2018. Chris then decided in 2021 that he wanted to sell 1 Bitcoin, worth $30 000, to go on holiday.

His calculations will be the following:

$30 000 – $11 000 = $19 000

Chris made a capital gain of $19 000. Therefore, he can pay capital gains tax on his gains of $19 000. However, Chris has kept his crypto for more than 12 months. Consequently, he will be entitled to claim a 50% capital gains tax discount on the $19 000 gain amount, amounting to $ 9 500. On that $ 9 500, he will be liable to pay capital gains tax.

Important to note

- The income tax, tax-free threshold is $18 200.

- If you purchase no more than AU$10000 of crypto to directly buy something else with crypto over a short or long period, you will be eligible for an exemption from capital gain tax.

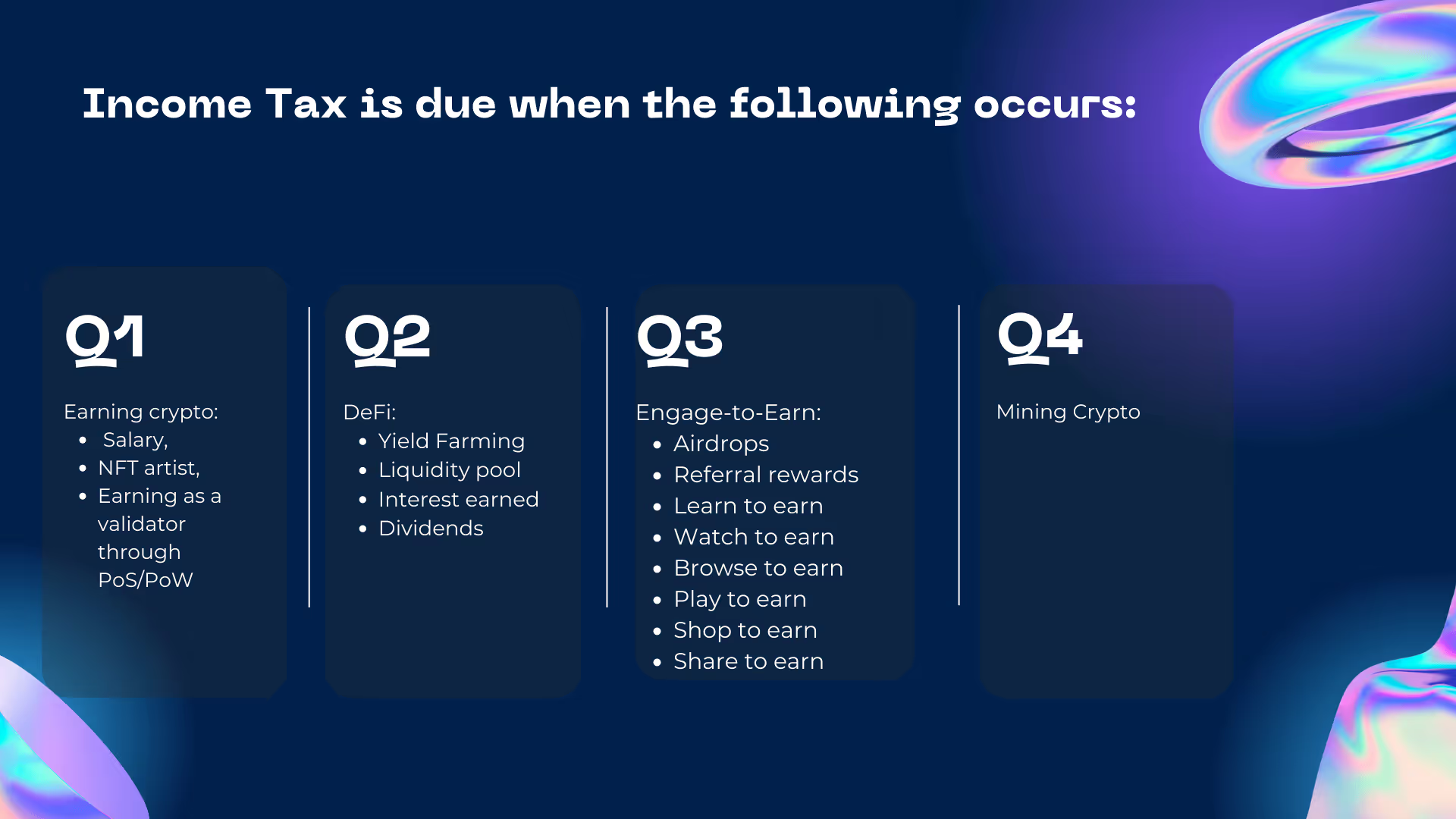

Income Tax on Crypto Profits

Crypto traders’ profits will classify as income, and it will attract Income Tax. However, this is not the only case where crypto is treated as income, and thus an Income Tax liability will arise for the taxpayer.

Staking is when you pledge your crypto assets to a blockchain network to increase the transactions on that blockchain. In this process, new coins are minted. Then, the income earned from minting those coins is distributed to participants.

An airdrop is a marketing method used to introduce new crypto projects to the market. The creators deposit these new coins into individual crypto traders’ wallets.

When seen as a business trade, income earned through staking, airdrops, and mining is taxed under income tax, with no capital gain tax.

Mining crypto assets as a business or trader leave you obligated to declare any profits made upon selling those crypto assets to the ATO. If you are mining as a hobby or business, consider specific factors. The ATO does mention these factors on their website.

As mentioned earlier, crypto assets received as income are subject to income tax, realised when received. If the value of that crypto increases before it is disposed of, it is also subject to capital gains tax.

Another way one can be taxed is when you earn or dispose of crypto assets through Decentralized Finance (DeFi).

Decentralised Finance (DeFi) has become quite popular amongst crypto enthusiasts. Decentralised Finance allows investors to have complete control over their assets when engaging in the crypto markets. Like many centralised financial organisations, Defi will enable you to trade, invest, loan, borrow, stake or deposit your digital assets through decentralised protocols.

The ATO has concluded that DeFi can be taxed either as Capital Gains Tax or Income tax. It all depends on how your income has been generated. The type of tax you will pay is determined by whether you earned or disposed of your crypto assets. Below are a few ways to acquire or dispose of crypto-assets through DeFi and how it is taxed.

Income Tax on DeFi

- Earn interest on Defi platforms

- Staking on Defi platforms

- Yield farming

- Play to earn

- Earning Liquidity tokens

Capital Gains Tax on DeFi

- Paying interest with Crypto

- Earning Liquidity Tokens

- Profits from Defi margin or options trading

- Selling or Swapping coins and tokens on DeFi networks

This Koinly DeFi tax guide gives an in-depth explanation of how Income can be generated through DeFi.

Capital loss

There is some relief when it comes to crypto taxes. For instance, if you have made losses instead of gains for the period. Your loss can be offset against the following year’s profits.

A capital loss occurs when the proceeds from the sale of your crypto are less than the initial amount paid to acquire it. A net capital loss can be deducted from another asset gain in Australia. Essentially, these losses can offset the gains made on crypto trades and investments. However, you may not remove a net capital loss from your other income.

If someone steals your crypto assets, you will not be held liable for taxes. But, of course, this needs to be proved first.

Stolen crypto

In Australia, unlike many other countries, you may be able to claim a capital loss if you lose your private key or have your crypto stolen. There are a few things you need to be able to present to the ATO to be able to claim a capital loss, including the following:

- The wallet address that the key belongs to

- When you acquired the key and when you lost it

- The cost of acquiring the stolen/lost cryptocurrency

- The fact that you controlled the wallet

- The amount of cryptocurrency at the time that you lost the key

- That you possess the hardware where the wallet is stored

- The transactions to the wallet from an exchange are directly linked to your identity

Crypto Reporting

Crypto taxing and reporting can be complex matters. Therefore, it is imperative to keep accurate records of your crypto-related transactions for five years. The ATO provides a list of documents you need to keep track of so that your tax calculations be the most accurate.

It is refreshing to see that the Australian government is lighter on crypto taxation compared to other countries worldwide.

Contact CountDeFi if you would like us to assist you in your crypto reporting needs.